25 oneri finanziari che potreste dover affrontare dopo la morte di una persona cara

Losing a loved one is already an emotional rollercoaster—but what many people don’t talk about is the financial burden that often comes with it. The bills don’t stop, the paperwork piles up, and suddenly, you’re dealing with expenses you never even considered.

From funeral costs and medical bills to legal fees and ongoing financial responsibilities, the hidden costs of losing someone can be overwhelming. And for those left behind, these financial burdens can add stress to an already devastating situation.

To help you prepare—or at least know what to expect—here are 25 financial challenges you may face after a loved one passes.

1. Funeral Costs

Funeral costs often catch families off guard, especially considering the sudden nature of planning. Many assume that life insurance will cover expenses, but this isn’t always the case. Funeral homes offer packages that can range significantly in price, leaving families in a financial bind. Imagine a grieving daughter, mid-40s, standing at a funeral home counter, her hands clutching a detailed bill. Each line item adds to the mounting pressure, from the casket to the service fees.

In many cultures, funerals are elaborate, involving multiple rituals and gatherings, each adding to the cost. The location of the service can also affect the price significantly, especially in urban areas where venue fees are higher. The emotional fog of grief can make it difficult to make decisions that could ease the financial burden.

Additional costs like obituary fees, flowers, and transportation often go unnoticed until it’s too late. These expenses can quickly add up, forcing families to dip into savings or even take out loans to manage the cost. Planning ahead and setting aside funds for such eventualities can provide some relief during an otherwise overwhelming time.

2. Outstanding Medical Bills

The shock of losing a loved one can be compounded by the discovery of outstanding medical bills. These can accumulate rapidly, especially if the deceased had been undergoing lengthy or intensive treatment.

Medical bills are not limited to immediate treatments but can include costs from months or even years prior. Insurance may cover a portion, but deductibles, co-pays, and uncovered services can leave substantial amounts unpaid. These lingering debts add to the emotional distress, as families must navigate the healthcare system’s complexities.

In some cases, negotiating with healthcare providers can result in reduced payments or manageable payment plans, offering some financial relief. However, the process requires time, patience, and a clear mind, which can be hard to muster during grief. Understanding the potential for these bills and seeking assistance from professionals early can prevent financial strain from spiraling out of control.

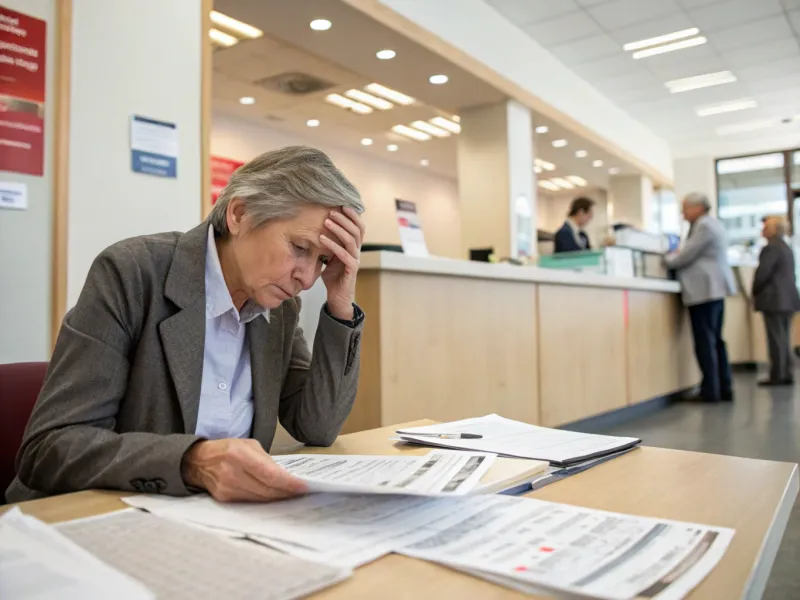

3. Estate Settlement Costs

Settling an estate is often more complicated and costly than anticipated. The legal complexities involved can be overwhelming, especially for those unfamiliar with probate proceedings.

Estate settlement involves appraising assets, paying off debts, and distributing the remaining assets according to the will. Legal fees, executor fees, and other administrative costs can quickly add up, depleting the estate’s value. In some cases, families may discover that the estate is insufficient to cover all obligations, requiring additional out-of-pocket expenses.

The probate process can be time-consuming, dragging on for months or even years, tying up assets that beneficiaries might need. Planning and understanding the process beforehand can mitigate these challenges. Consulting with estate professionals and setting up living trusts or other financial arrangements can simplify the process, reduce costs, and ensure a smoother transition of assets.

4. Income Loss

The loss of a loved one often comes with the stark reality of income loss, especially if they were a primary earner.

This immediate impact can be exacerbated by the sudden need to adjust budgets, cut non-essential expenses, and find alternative income sources. The transition can be jarring, particularly for families unprepared for such a drastic change. Life insurance might offer temporary relief, but it may not fully replace the long-term financial contributions of the deceased.

Beyond the immediate loss, future plans and savings goals may be disrupted, affecting education funds, retirement savings, and other long-term financial strategies. Seeking financial advice early and exploring options like survivor benefits, part-time work, or retraining for new employment can help bridge the gap. Developing a sustainable financial plan ensures that the family can maintain a semblance of normalcy despite the significant change.

5. Inheritance Taxes

Inheritance taxes can be an unexpected financial burden, surprising many who assume that inherited assets are tax-free.The realization that a portion of the inheritance must be paid in taxes can dampen the relief of receiving financial support.

The tax laws vary significantly depending on the jurisdiction, and understanding them requires careful attention to detail. Some regions impose hefty taxes on property, cash, or stocks, potentially reducing the net value of the inheritance. For beneficiaries unprepared for these costs, the burden can lead to financial strain.

Professional tax advisors can offer guidance and potentially identify ways to minimize tax liabilities. Early estate planning, including setting up trusts or gifting assets prior to death, can reduce or even eliminate inheritance taxes. Educating oneself about local tax laws and preparing accordingly ensures that beneficiaries can maximize the benefits of their inheritance, easing the financial transition after a loss.

6. Legal Fees

Legal fees can accumulate quickly when settling a loved one’s affairs, creating an additional financial burden. Navigating the legal system requires both time and money, adding to the emotional toll of loss.

Whether dealing with contested wills, probate proceedings, or other legal matters, these costs can be substantial. Each hour spent with an attorney adds to the bill, and unexpected legal challenges can prolong the process, further inflating costs. For many, these expenses come as a shock, compounding the grief with financial worry.

To minimize these costs, it’s advisable to consult with an attorney experienced in estate law early in the process. They can provide guidance on how to proceed efficiently, potentially reducing the time and money spent. Preparing legal documents well in advance and ensuring clear, conflict-free wills and estate plans can also mitigate the risk of costly legal battles.

7. Credit Card Debt

Credit card debt left by a deceased loved one can present an unexpected challenge. The realization that these debts don’t simply vanish with their loved one can be distressing.

In many cases, the estate is responsible for settling outstanding debts, but if the estate lacks sufficient funds, the burden may fall on family members. Joint account holders or co-signers may find themselves liable for remaining balances. This can be particularly troubling for those already managing their own financial obligations.

Understanding the terms and conditions of credit agreements is crucial. Reach out to credit card companies to discuss possible repayment plans or debt forgiveness options. Legal advice can also be beneficial, helping family members understand their rights and responsibilities regarding outstanding debts. Taking proactive steps to manage and settle these accounts can alleviate some of the financial stress during an emotionally challenging time.

8. Mortgage Payments

Mortgage payments can quickly become a pressing concern after a loved one’s death, particularly if they were the primary or sole contributor. The absence of income can place the family home at risk.

Even if the mortgage was paid regularly in the past, the sudden loss of income can make it difficult to keep up with payments. Life insurance or mortgage protection insurance policies can provide temporary relief, but they may not cover long-term needs. For many families, the fear of losing their home adds a significant layer of stress to an already difficult time.

Exploring options such as refinancing, modifying loan terms, or even selling the property may be necessary. Consulting with financial advisors and mortgage specialists can provide insights and solutions tailored to the family’s specific situation. Taking action promptly can prevent foreclosure and help the family retain their home, easing the transition after loss.

9. Unpaid Loans

Unpaid loans left behind by a deceased loved one can become an unexpected financial burden. The responsibility of repaying these debts can fall heavily on the shoulders of survivors.

Often, the estate is tasked with settling outstanding loans, but when assets are insufficient, family members, particularly co-signers or guarantors, may find themselves liable. This can lead to financial strain, especially for those unprepared for such responsibilities. Understanding the terms of the loan and the implications for survivors is crucial.

Communicating with lenders early can help explore options for managing these debts. Some institutions offer repayment plans or debt forgiveness in certain circumstances. Legal advice can also be beneficial, providing clarity on rights and responsibilities. Taking these steps can help alleviate some of the financial pressure, allowing families to focus on healing and moving forward.

10. Unfulfilled Subscriptions

In today’s digital age, unfulfilled subscriptions can become a surprising financial burden after a loved one’s passing.

From streaming services to online memberships, many people accumulate numerous subscriptions over time. In the hustle of daily life, it’s easy to overlook these small, recurring charges. However, when added up, they can represent a significant expense, especially if they remain unnoticed for months.

The process of canceling these subscriptions can be time-consuming and often requires access to accounts and passwords that were solely managed by the deceased. Taking inventory of all active subscriptions and promptly canceling or transferring them can prevent unnecessary financial drain. This task might seem minor amidst larger financial challenges, but it’s an actionable step that can provide immediate relief and prevent future complications.

11. Property Maintenance Costs

Property maintenance costs can escalate quickly, becoming an unforeseen financial challenge after a loved one’s death.

The upkeep of a property requires regular attention, from lawn care to structural repairs. If the deceased was primarily responsible for these tasks, the sudden shift in responsibilities can be daunting. Hiring professionals to handle maintenance can lead to unplanned expenses, especially if the property was not well-maintained before.

Furthermore, neglecting maintenance can lead to depreciation in property value, affecting potential future sales. Understanding the scope of necessary tasks and budgeting for them helps manage these costs effectively. Engaging with local service providers and comparing quotes ensures that maintenance remains affordable. Recognizing the need for ongoing care enables families to preserve their loved one’s property as they navigate this challenging time.

12. Utility Bills

Utility bills, often overlooked, can become a significant financial burden following a loved one’s passing. Utilities are essential, yet their costs can quickly accumulate, particularly if the deceased was the primary contributor to household expenses. In the absence of their income, these recurring charges demand attention, requiring either payment or strategic reduction.

Reviewing each utility service and identifying opportunities for savings is a practical step. Negotiating with providers or switching to alternative plans can result in lower costs. Additionally, implementing energy-saving measures reduces consumption, providing long-term financial relief. By taking control of utility expenses, families can alleviate some of the financial pressure, allowing them to focus on healing and rebuilding after loss.

13. Childcare Expenses

Childcare expenses can escalate unexpectedly after a loved one’s passing, particularly if the deceased was a primary caregiver.

The sudden need for additional childcare services can strain an already tight budget. For working parents, the loss of a caregiver means finding reliable and affordable alternatives quickly. This urgency can lead to increased costs, as families might have to settle for pricier options to ensure quality care.

Balancing work and family life becomes even more challenging, often requiring adjustments in work schedules or even career changes. Exploring community resources, such as after-school programs or family assistance, can provide some financial relief. By proactively seeking solutions and planning for childcare needs, families can navigate this transitional period more smoothly, focusing on providing stability for their children during a time of change.

Vedi anche: 30 storie sconvolgenti di coniugi lasciati fuori dal testamento

14. Pet Care Costs

Pet care costs can become an unexpected financial burden after a loved one’s passing, especially if the deceased was primarily responsible for their care.

Pets require regular attention and care, including veterinary visits, food, grooming, and more. The sudden responsibility of these expenses can catch families off guard, as they may not have budgeted for such costs beforehand. This can lead to financial strain, forcing families to make difficult decisions regarding their pet’s care.

Exploring options such as pet insurance or community resources for support can provide some financial relief. Additionally, finding affordable service providers and seeking advice from fellow pet owners can help manage costs effectively. Recognizing the need for ongoing pet care and planning accordingly ensures that beloved pets continue to receive the attention they deserve during this transitional time.

15. Creditors’ Claims

Creditors’ claims can present a surprising financial burden after a loved one’s death. Imagine a stack of creditor letters on a desk, and a middle-aged man in his 50s reading them with concern. Each letter represents a demand for payment, adding to the financial complexities faced by grieving families.

When someone passes away, creditors may file claims against the estate to recover debts. This process can be lengthy and complicated, involving legal proceedings that require time and expertise. If the estate lacks sufficient assets, beneficiaries may find themselves facing unexpected financial obligations.

Understanding the rights and responsibilities regarding creditors’ claims is crucial. Consulting with legal professionals can provide clarity and guidance, helping families navigate this challenging process. By addressing creditors’ claims promptly and effectively, families can minimize financial stress and focus on healing and moving forward after loss.

16. Legal Guardianship Fees

Legal guardianship fees can become an unexpected financial burden after a loved one’s passing, particularly if minor children are involved.

Designating a legal guardian involves court proceedings, legal documents, and associated fees. These costs can add up quickly, especially if disputes arise or additional legal services are required. For many families, the financial burden of securing guardianship adds to the emotional stress of ensuring the children’s well-being.

Understanding the legal process and seeking professional guidance early can help manage these costs effectively. Establishing guardianship plans and involving all relevant parties in discussions ensures a smoother transition. By preparing in advance and navigating the legal landscape efficiently, families can focus on providing stability and support for the children during this challenging time.

17. Sentimental Asset Valuation

Valuing sentimental assets such as jewelry, art, or collectibles can be a sensitive financial burden. These items often hold emotional value beyond their monetary worth, complicating decisions about whether to keep, sell, or distribute them.

Engaging a professional appraiser can provide clarity but comes at a cost. Alternately, family discussions may help strike a balance between financial needs and emotional attachments.

Consider setting aside particularly cherished items or splitting collections to satisfy both financial and sentimental considerations.

18. Home Repairs

Home repairs can become an unexpected financial burden after a loved one’s passing, particularly if the deceased was responsible for maintenance.

The upkeep of a home requires regular attention, from structural repairs to routine maintenance. If neglected, these issues can escalate, leading to costly repairs that strain the family’s budget. For many, the realization of these responsibilities adds to the emotional and financial challenges of losing a loved one.

Understanding the property’s condition and prioritizing necessary repairs helps manage costs effectively. Engaging with local contractors for quotes and exploring community resources for assistance can provide financial relief. By addressing these repairs promptly, families can maintain their home’s value and create a safe, comfortable environment during this difficult time.

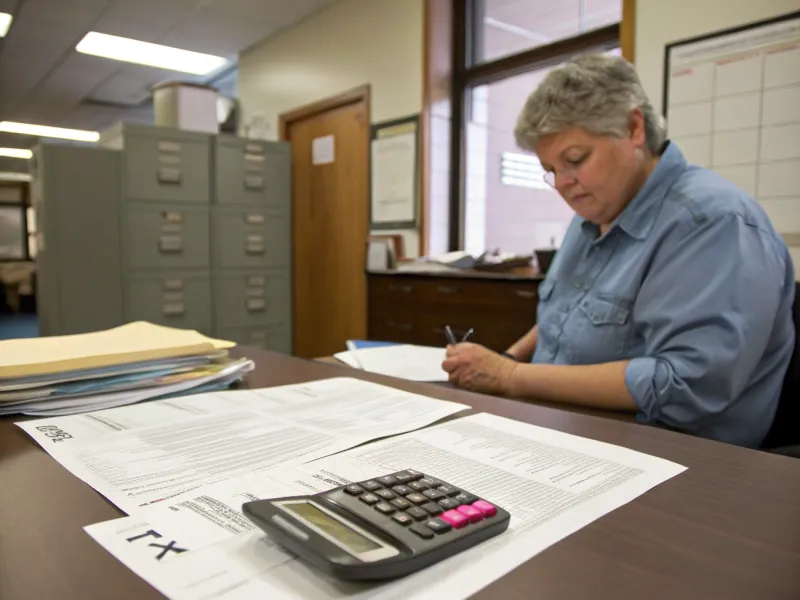

19. Unpaid Taxes

Unpaid taxes can become an unforeseen financial burden after a loved one’s passing. When someone passes away, any outstanding tax obligations must be addressed, often requiring payment before the estate is settled. These obligations can include income taxes, property taxes, or other government levies. For many families, the complexity of tax laws and the immediacy of these financial demands add to the stress of grieving.

Consulting with tax professionals can provide clarity and guidance, helping families understand their responsibilities and explore options for managing these debts. Early planning and organization, including gathering necessary documents and understanding applicable laws, can prevent further complications. By addressing unpaid taxes efficiently, families can focus on healing and moving forward after loss.

20. Business Obligations

Business obligations can become an unexpected financial burden after a loved one’s passing, especially if they were a business owner or partner.

The sudden loss of a key individual can disrupt operations, affecting cash flow and leading to increased financial pressure. In some cases, existing business debts or contractual obligations may require immediate attention, adding to the burden. For those left behind, the responsibility of managing these obligations can be overwhelming.

Understanding the business’s financial position and seeking professional advice can offer guidance and support. Exploring options such as restructuring, selling, or even liquidating the business may be necessary to alleviate financial strain. By addressing business obligations promptly and effectively, families can focus on healing and rebuilding, ensuring the continuation of the loved one’s legacy.

21. Student Loans

Student loans can become a surprising financial burden after a loved one’s passing, particularly if the deceased was a co-signer.

Student loans generally do not disappear upon the borrower’s death, especially if a co-signer is involved. This responsibility can fall on family members, adding to their financial stress. Understanding the terms and conditions of these loans is essential, as it affects the repayment obligations of survivors.

Reaching out to loan servicers to discuss options such as deferment, forbearance, or even loan forgiveness in certain cases can provide some relief. Legal advice may also be beneficial, offering clarity on rights and responsibilities. By addressing student loans proactively, families can alleviate financial pressure and focus on supporting each other during this challenging time.

22. Funeral Catering Costs

Funeral catering costs can become a surprising financial burden after a loved one’s passing, especially if the deceased requested an elaborate gathering. Picture a catering setup at a funeral, with a planner in their 30s diligently organizing every detail.

The desire to honor a loved one’s memory with a meaningful celebration can lead to significant expenses. Catering services, including food, beverages, and staff, can quickly add up, placing additional stress on grieving families. Often, these costs are not anticipated, leaving families scrambling to find funds.

Understanding the options available and setting a realistic budget can help manage these expenses. Exploring community support or opting for simpler arrangements may provide financial relief. By planning carefully and considering all available resources, families can create a meaningful gathering without compromising their financial stability.

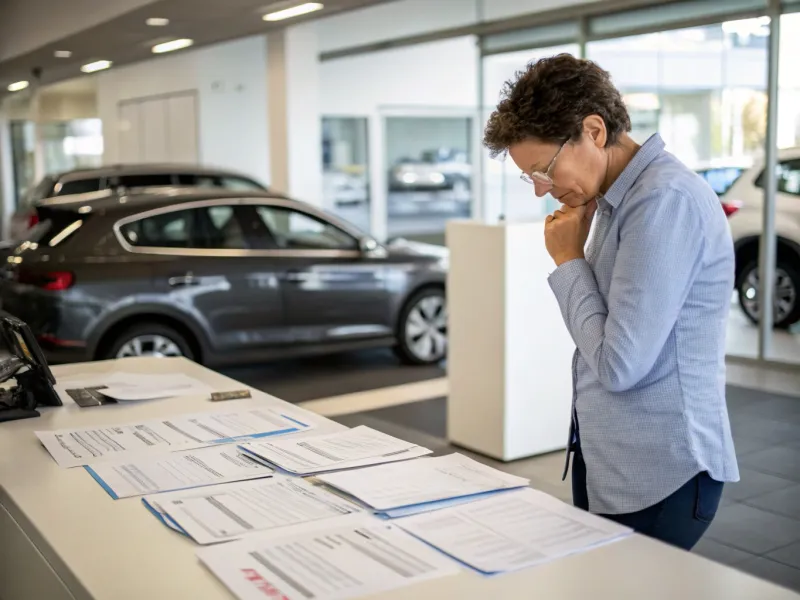

23. Vehicle Loans

Vehicle loans can become an unexpected financial burden after a loved one’s passing, particularly if the deceased was the primary borrower.

The sudden responsibility of managing vehicle loans can catch families off guard, especially if they were not prepared for such obligations. If the estate lacks sufficient assets to cover the loan, the burden may fall on surviving family members or co-signers, leading to financial strain.

Communicating with lenders and understanding loan terms is crucial to exploring options for managing these debts. Some lenders may offer payment plans or loan restructuring, providing temporary relief. Legal advice can also be beneficial, offering clarity on rights and responsibilities. By taking proactive steps to address vehicle loans, families can alleviate some of the financial stress and focus on healing and rebuilding after loss.

24. Personal Loans

Personal loans can become an unexpected financial burden after a loved one’s passing, especially if the deceased had outstanding debts.

Understanding the terms of personal loans and the responsibilities of survivors is crucial. Often, the estate is responsible for settling these debts, but if assets are insufficient, family members may find themselves liable. This can compound the emotional distress of losing a loved one, adding financial worry to the mix.

Reaching out to lenders to discuss repayment options or potential forgiveness can provide some relief. Legal advice may also be beneficial, offering clarity on rights and responsibilities. By taking proactive steps to address personal loans, families can alleviate financial pressure and focus on supporting each other during this challenging time.

25. Digital Assets and Accounts

Digital assets and accounts can become a surprising financial burden after a loved one’s passing. In today’s digital world, many people accumulate numerous online accounts and assets, from social media to online banking. Managing these accounts after a loved one’s death can be time-consuming and complex, especially if access information is not readily available. The financial implications of unclaimed assets or unresolved accounts can add to the stress of grieving families.

Taking inventory of all digital assets and accounts, and seeking advice on how to manage or transfer them effectively is essential. Engaging with digital service providers and understanding their policies on account management after death can prevent financial complications. By addressing digital assets proactively, families can alleviate some of the financial stress and focus on healing and rebuilding after loss.