37 Risky Boomer Money Moves That Might Leave Their Kids Empty-Handed

We’re about to have a heart-to-heart about some of the eyebrow-raising decisions our beloved Baby Boomers are making. Now, don’t get me wrong—I love my parents’ generation, but sometimes, their choices leave me scratching my head.

You might wonder how these decisions impact not just our lives, but also the legacy they’ll leave behind. So, let’s dive into this candid chat about 37 decisions that might just leave their kids with, well, a whole lot of nothing.

1. Ignoring Estate Planning

Estate planning—sounds fancy, right? But let me tell you, it’s not all about trust funds and mansions. It’s about making sure your hard-earned assets don’t get lost in legal mumbo jumbo. Yet, many Boomers seem to think they’ll live forever (we wish!) and put off this crucial task. Picture this: a middle-aged child, puzzled, staring at piles of dusty paperwork, wondering what on earth to do next.

Without a will or a clear plan, families can find themselves in a maze of legal chaos. I’ve heard stories where siblings end up in court, battling over who gets Grandma’s prized china. It’s not just about the stuff—it’s the emotional toll it takes. A little planning goes a long way, and it could mean the difference between a smooth transition and a family feud.

So, if you’re a Boomer reading this, or a concerned child of one, consider having ‘the talk.’ It might be a bit awkward, but trust me, future-you will thank you. A stitch in time saves nine, as they say, and in this case, saves a lot of heartache too.

2. Overspending on Luxury

Oh, the allure of shiny new things! Who can resist the temptation of a luxury car or a dream vacation to the Maldives? Boomers, it seems, have a penchant for indulging in life’s little luxuries, and who can blame them? But these expenses can add up faster than you can say ‘retirement fund.’

Now, I’m all for enjoying the fruits of one’s labor, but there’s a fine line between treating yourself and jeopardizing your financial future. Imagine an elderly couple gleefully browsing a showroom of luxury cars, but with a subtle shadow of doubt lingering. The kids are wondering if there’ll be anything left for their college tuition or family emergencies.

It’s not about denying pleasures but finding a balance. Perhaps it’s time for a gentle nudge to remind them that experiences don’t always have to come with a hefty price tag. Sometimes, the best memories are made in the backyard with a barbecue, not a five-star resort. Let’s make sure those indulgences don’t come at the cost of a secure future for everyone involved.

3. Rejecting Technology

Technology—it’s a love-hate relationship for many Boomers. Picture a 70-year-old gentleman, staring at a smartphone as if it’s an alien artifact, while his tech-savvy grandkid attempts to explain apps. This generational gap can lead to missed opportunities and, believe it or not, financial strain.

By shunning online banking, investing, or even digital communication, Boomers might find themselves out of the loop. It’s not just about staying connected with family, but also about managing finances efficiently and avoiding scams. There’s so much potential in those little devices, but only if they’re willing to take the plunge.

Encouraging Boomers to embrace technology isn’t just about convenience—it’s about empowerment. With a bit of patience and guidance, they can unlock a world of possibilities. So, next time you’re together, perhaps gently coax them into joining a tech class or simply exploring a new app. Who knows? They might just become the next tech aficionado in the family!

4. Neglecting Healthcare Costs

Healthcare—an ever-looming expense that seems to creep up on us all. Picture this: a 65-year-old woman sitting in a doctor’s office, her face a mix of concern and confusion as she reviews a stack of medical bills. Healthcare costs are rising, yet many Boomers are caught off guard, failing to plan adequately for these inevitable expenses.

Ignoring these costs can lead to financial distress not only for them but also for their children, who may have to step in and help. It’s a tough spot to be in, feeling the weight of your parents’ medical bills while trying to manage your own finances. The key is in planning and understanding the options available.

Encourage conversations about health insurance, long-term care, and preventive measures. This isn’t just important—it’s essential. By addressing these issues head-on, Boomers can alleviate some of the financial burdens and ensure they’re not leaving their kids with unexpected debts. Remember, health is wealth, and a bit of foresight can go a long way in preserving both.

5. Investing in Risky Ventures

The thrill of a new business venture can be intoxicating. Imagine a 68-year-old man, filled with enthusiasm, signing papers at a start-up meeting, surrounded by eager entrepreneurs half his age. While investing can be a great way to grow wealth, it’s not without its pitfalls, especially for Boomers who may not have as much time to recover from financial missteps.

Risky investments can drain retirement savings faster than anticipated, leaving little for the next generation. It’s not uncommon for Boomers to get swept up in the promise of high returns, neglecting the potential downsides. The fear of missing out can sometimes overshadow prudent decision-making.

Encouraging Boomers to seek advice from financial advisors and to diversify their portfolios can mitigate risks. It’s essential to balance excitement with caution, ensuring that these investments don’t jeopardize their financial security or that of their children. After all, smart investing is not just about the potential gains but also about protecting what you’ve worked hard to achieve.

6. Holding onto Large Homes

Ah, the family home—a place filled with memories, laughter, and maybe a few quirky design choices from the ’70s. Picture a spacious, slightly outdated house, where an elderly couple sits, reminiscing about days gone by. It’s heartwarming, but as lovely as it is, holding onto a large home can be financially draining for Boomers.

Maintenance, taxes, and utilities can eat away at their savings, leaving less for their children when the time comes. The emotional attachment is understandable, but downsizing could be a wise financial move, freeing up resources for other important aspects of life.

Perhaps it’s time to consider options like selling or renting out unused portions of the home. Encouraging Boomers to explore these possibilities might open up new chapters for them and ensure that their kids aren’t left with the burden of maintaining a property that no longer suits their needs. Sometimes, letting go of the past is the best way to embrace the future.

7. Taking on Too Much Debt

Debt—a word that sends shivers down the spine. Imagine a middle-aged couple, frazzled, surrounded by piles of credit card statements at their kitchen table. It’s a scene all too familiar for many Boomers who find themselves juggling debt well into retirement.

Whether it’s from home renovations, helping out family, or simply indulging in a few too many treats, debt can snowball quickly. The stress of managing repayments can be overwhelming, affecting not only their financial well-being but also their quality of life.

Helping Boomers understand the importance of budgeting and prioritizing expenditures can steer them away from this slippery slope. It’s about making informed choices and perhaps seeking guidance from financial advisors to manage and reduce debt effectively. By doing so, they can ease the pressure and ensure they aren’t passing on financial burdens to their children. Remember, it’s never too late to take control and find a path to financial freedom.

8. Not Updating Beneficiaries

Beneficiaries—those people you lovingly name to inherit your treasures. But here’s the kicker: many Boomers forget to keep this crucial information up to date. Picture a 72-year-old woman, peering at a dust-covered file labeled ‘Beneficiaries,’ with a look of bewilderment on her face.

Life changes—marriages, births, divorces—and so should beneficiary designations. Failing to update these can lead to unintended heirs or legal wrangling, leaving children with a legacy of headaches. It’s a small oversight that can lead to big complications.

Encouraging Boomers to regularly review and update their beneficiary information is a simple yet effective way to avoid potential pitfalls. It’s about taking a few moments now to ensure their wishes are honored and their loved ones aren’t left tangled in red tape. A little attention to detail can go a long way in preserving peace of mind for everyone involved.

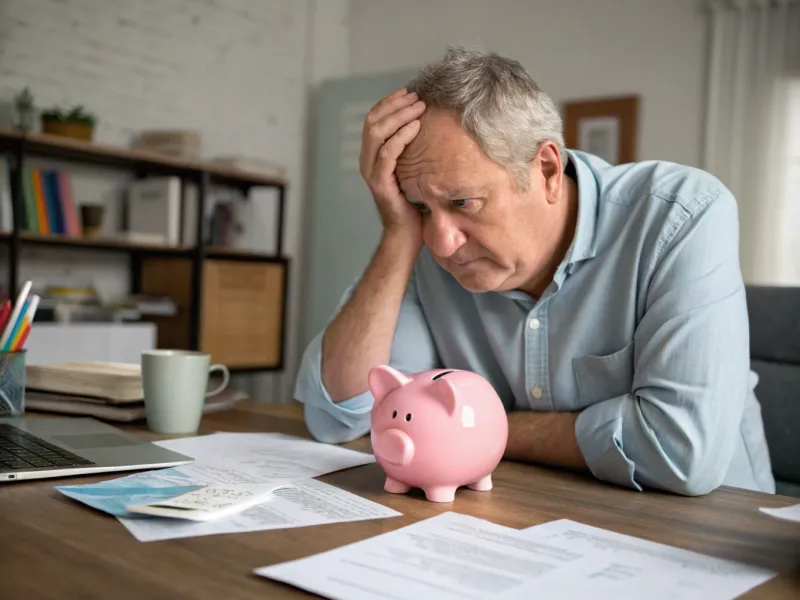

9. Neglecting Retirement Savings

Retirement—a time to put your feet up and enjoy the fruits of your labor. But for some Boomers, the reality can be quite different. Imagine a 60-year-old man, gazing anxiously at an empty piggy bank, wondering where all the time—and money—went.

Many Boomers find themselves facing retirement with less savings than they’d hoped, often due to lack of planning or unexpected life events. It’s a stressful situation that not only affects them but can also place a burden on their children, who might feel compelled to assist financially.

Encouraging Boomers to reassess their savings plans, seek professional advice, and make informed decisions can help bridge the gap. It’s never too late to start or adjust retirement strategies, ensuring a more secure future and peace of mind. The key is in taking action sooner rather than later, so retirement can be a time of relaxation, not worry.

10. Ignoring Inflation

Inflation—it creeps up on you like a mischievous cat. Picture a 65-year-old man, staring in disbelief at a grocery receipt, the prices seemingly climbing with each passing day. Inflation is a silent thief, slowly eroding purchasing power and affecting long-term financial plans.

For Boomers, ignoring inflation can mean their savings don’t stretch as far as they’d hoped. This oversight can lead to financial strain, not just for them but potentially for their children as well. It’s crucial to factor in inflation when planning for retirement and other future expenses.

Encouraging Boomers to consult financial advisors and adjust their strategies can help protect against this economic phenomenon. It’s about staying informed and proactive, ensuring that their nest egg remains robust and capable of supporting them through the years. After all, knowledge is power, and understanding inflation is a key part of safeguarding one’s financial future.

11. Not Preparing for Long-Term Care

Long-term care—it’s one of those topics nobody wants to talk about, but it’s oh-so-important. Picture a 70-year-old woman, worry etched on her face, discussing care options with a family member. As Boomers age, the likelihood of needing long-term care increases, yet many are not prepared for the associated costs.

Ignoring this aspect can lead to financial stress, as the expense of long-term care can quickly deplete savings meant for retirement or inheritance. It’s not just a financial burden but an emotional one, as families scramble to find suitable care options.

Encouraging open discussions about long-term care insurance and other planning measures can alleviate some of these pressures. It’s about being proactive and ensuring there are funds set aside to cover potential needs. By addressing this head-on, Boomers can safeguard their financial future and that of their children, offering peace of mind for everyone involved.

12. Keeping Outdated Investments

Ah, the world of investments—ever-changing and sometimes downright confusing. Imagine a 68-year-old man, holding onto dusty old stock certificates, his expression a mix of nostalgia and bewilderment. Many Boomers find themselves clinging to outdated investments, often because they don’t know where to begin with modern financial instruments.

Holding onto these can mean missed opportunities for growth, as the market evolves and new avenues arise. It’s not just about the potential gains lost but also the financial security that could have been enhanced with more current strategies.

Encouraging Boomers to consult with financial experts and explore new investment opportunities can open up a world of possibilities. It’s about embracing change and understanding that sometimes, letting go of the past is the best way to secure the future. By staying informed and adaptable, they can ensure their financial portfolio remains robust and beneficial for themselves and their children.

13. Focusing on Material Possessions

Material possessions—those beloved treasures that often come with a side of clutter. Picture an elderly couple surrounded by mountains of collected items, their living room a testament to years of accumulation. Many Boomers find themselves in this scenario, valuing material things over financial security.

While it’s understandable to cherish memories and prized possessions, it’s important to strike a balance. Clinging to material wealth can mean less attention to financial planning and saving, ultimately leaving less for the next generation.

Encouraging Boomers to evaluate what’s truly important can help them prioritize their financial future. It might be time to declutter, sell or donate unused items, and focus on experiences and opportunities that enhance life without compromising financial stability. By shifting their focus, they can ensure they’re leaving a legacy of memories, not just things, for their children.

14. Ignoring Environmental Impact

Environmental impact—it’s a topic that seems to resonate more with younger generations. Picture a 65-year-old woman, her brow furrowed as she reads about climate change and ecological issues on a tablet. Many Boomers, having grown up in a different era, might overlook the environmental consequences of their choices.

Ignoring these impacts can lead to decisions that not only affect their own environment but also the planet that will be inherited by their children and grandchildren. While not directly financial, these decisions have long-term implications that can indirectly affect economic stability and quality of life.

Encouraging Boomers to become more environmentally conscious can have a ripple effect. It’s about understanding that small changes in lifestyle and consumption can lead to significant positive outcomes. By embracing sustainability and eco-friendly practices, they can contribute to a healthier planet and ensure a better future for the generations to come.

15. Avoiding Financial Education

Financial education—it’s the foundation of sound money management, yet many Boomers shy away from it. Picture a 70-year-old man, a financial planning book gathering dust on his desk, while he kicks back watching TV. Avoiding financial education can lead to uninformed decisions, missed opportunities, and ultimately, financial strain.

Without a strong understanding of financial concepts, Boomers may find themselves struggling with budgeting, saving, and investing. This not only impacts their own financial health but can also leave their children with unexpected burdens.

Encouraging Boomers to engage in financial courses or seek advice from reputable sources can empower them to make informed decisions. It’s about shifting the mindset from avoidance to proactive learning, ensuring they have the tools needed to navigate their financial future. Knowledge, after all, is power, and it’s never too late to learn.

16. Relying on Social Security Alone

Social Security—so many see it as the safety net for their golden years, yet relying solely on it can be a risky game. Picture a 66-year-old man, furrowing his brow as he calculates expenses, Social Security statement in hand. The reality is that Social Security alone may not cover all the costs of retirement, leaving Boomers in a precarious position.

Depending entirely on this program can mean a lack of flexibility and financial freedom, especially as living expenses rise. This can place additional financial stress on their children, who might have to step in to help fill the gaps.

Encouraging Boomers to explore additional sources of income, such as part-time work or investments, can provide a more stable financial foundation. It’s about understanding the limitations of Social Security and planning accordingly. By doing so, they can ensure a more comfortable retirement and alleviate potential financial burdens on the next generation.

17. Falling for Scams

Scams—they lurk in the shadows, waiting to pounce on unsuspecting victims. Imagine an elderly woman in her late 70s, distressed after receiving a fraudulent call promising riches beyond belief. Many Boomers find themselves targets of scams, often losing substantial amounts of money in the process.

These scams can devastate financial security, leaving little for their children and affecting their quality of life. The emotional toll can be just as damaging, fostering feelings of betrayal and vulnerability.

Educating Boomers about recognizing scam tactics and encouraging vigilance can be a powerful tool in prevention. It’s about fostering open communication and creating awareness, ensuring they feel equipped to handle suspicious encounters. By doing so, they can protect their hard-earned assets and maintain their financial well-being.

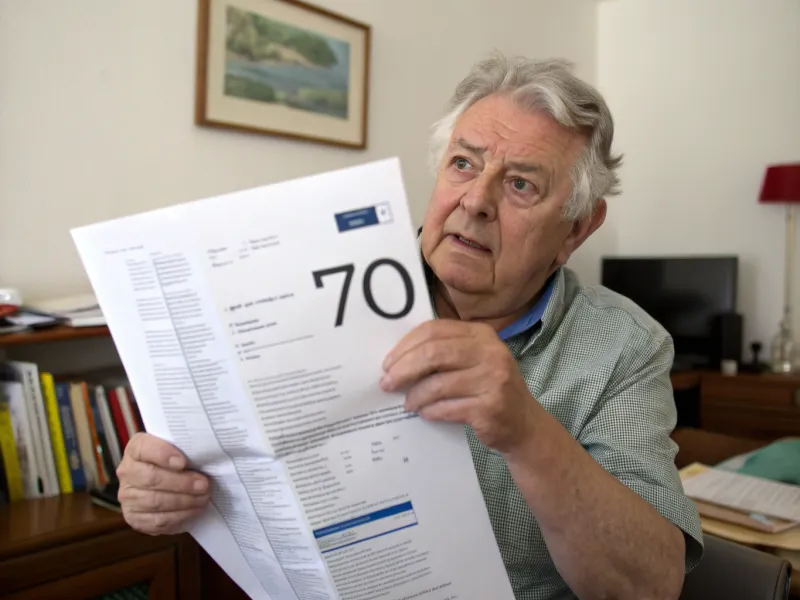

18. Underestimating Life Expectancy

Life expectancy—it’s on the rise, but many Boomers still plan for shorter retirements. Picture a 68-year-old woman, eyes wide with surprise as she reads an article about increasing life expectancy. Underestimating how long they might live can lead to financial shortfalls during retirement years, leaving them, and potentially their children, in a bind.

Many don’t account for the extended time they may need financial support, leading to depleted savings and increased reliance on family. It’s a scenario that’s becoming more common as healthcare advances prolong life.

Encouraging Boomers to adjust their financial plans with a longer life expectancy in mind is crucial. It’s about planning for the long haul and ensuring their savings can sustain them comfortably. By doing so, they can enjoy their golden years without the looming worry of outliving their resources.

19. Ignoring Legal Advice

Legal advice—often perceived as complicated and expensive, yet oh-so-necessary. Picture a 70-year-old man, arms crossed, dismissing a lawyer’s advice with a stubborn look. Many Boomers shy away from seeking legal counsel, opting to handle matters themselves, often to their detriment.

Ignoring legal advice can lead to costly mistakes, especially concerning estate planning, taxes, and property laws. The consequences can ripple through generations, leaving children with legal battles and financial burdens.

Encouraging Boomers to seek professional legal advice ensures they make informed decisions. It’s about recognizing the value of expertise and not letting pride or misconceptions stand in the way. By doing so, they can protect their assets and ensure a smoother transition of wealth and responsibilities to their children.

20. Delaying Retirement Planning

Retirement planning—it’s crucial, yet many Boomers find themselves putting it off until the last minute. Picture a 60-year-old man, stress etched on his face, as he glances at a calendar, realizing time is slipping away. Delaying retirement planning can lead to inadequate savings and a less secure financial future.

Without a solid plan, Boomers may find their retirement dreams compromised, affecting not only their lives but also putting pressure on their children to help fill the gaps. It’s a cycle that can be avoided with timely and proactive planning.

Encouraging Boomers to start or revisit their retirement plans can make a significant difference. It’s about taking control and ensuring they have the resources needed to enjoy their later years comfortably. By addressing this now, they can avoid future financial stress and leave a more secure legacy for their children.

21. Avoiding Conversations About Finances

Finances—a topic that can be as taboo as politics or religion at family gatherings. Picture an awkward family dinner, where no one dares to broach the subject of financial plans. Avoiding these conversations can lead to misunderstandings and missed opportunities for alignment and support.

Many Boomers shy away from discussing finances with their children, often out of a desire to protect them or simply discomfort with the topic. However, this silence can lead to uncertainty and unexpected burdens when plans aren’t clearly communicated.

Encouraging open, honest discussions about financial goals and expectations can bridge the gap between generations. It’s about creating a space where everyone feels comfortable sharing and contributing to a collective plan. By doing so, Boomers can ensure their wishes are understood and their children are prepared for the future.

22. Not Diversifying Investments

Diversification—it’s a buzzword in the investment world for a reason. Picture a 65-year-old man, eyes wide as he watches market graphs fluctuate wildly on his computer screen. Not diversifying investments can lead to significant financial pitfalls, especially for Boomers who may not have the time to recover from losses.

Relying too heavily on a single type of investment can expose them to unnecessary risk, potentially affecting their financial security and that of their children. It’s about finding a balance and spreading investments across various asset classes to mitigate risk.

Encouraging Boomers to consult financial professionals and diversify their portfolios can help safeguard against market volatility. It’s about understanding that a well-rounded investment strategy is key to ensuring financial stability and growth. By doing so, they can protect their assets and provide a more secure financial future for themselves and their children.

23. Holding Onto Unprofitable Businesses

Businesses—often seen as the fruit of one’s labor, but what happens when they’re no longer viable? Picture an elderly couple, worry etched on their faces as they stand in an empty shop, clinging to a business that’s seen better days. Many Boomers find themselves in this predicament, holding onto unprofitable businesses out of nostalgia or hope for a turnaround.

Continuing to invest time and money into a failing venture can drain their finances and leave little for their children. It’s a tough decision, but sometimes the best move is to cut losses and explore new opportunities.

Encouraging Boomers to assess their business ventures honestly and seek advice from professionals can help them make informed decisions. It’s about recognizing when it’s time to let go and finding new paths that contribute to financial security. By doing so, they can protect their assets and ensure a more stable future for themselves and their children.

24. Not Keeping Up with Housing Market Trends

The housing market—it’s nothing if not unpredictable. Picture a 68-year-old woman, taken aback as she browses real estate listings with skyrocketing prices. Many Boomers find themselves out of touch with current housing trends, potentially missing out on opportunities to maximize their property’s value.

Ignoring market trends can lead to financial losses or missed chances to downsize or relocate advantageously. This can affect their overall financial health and limit the inheritance left for their children.

Encouraging Boomers to stay informed about housing market trends can provide them with valuable insights. It’s about making strategic decisions that enhance their financial position and ensure a more secure future. By doing so, they can optimize their real estate assets and leave a lasting legacy for their children.

25. Overlooking Tax Implications

Taxes—often the bane of our financial lives, yet so crucial to understand. Picture a 70-year-old man, shock etched on his face as he sits at a cluttered desk, a hefty tax bill in hand. Many Boomers overlook the tax implications of their financial decisions, leading to unexpected expenses and diminished savings.

Ignoring these can lead to financial strain, affecting not only their quality of life but also the legacy they leave for their children. It’s about understanding the tax landscape and planning accordingly to minimize liabilities.

Encouraging Boomers to consult with tax professionals and stay informed about current tax laws can help them navigate this complex field. It’s about making informed choices that protect their assets and ensure a smoother financial journey. By doing so, they can safeguard their wealth and provide a more secure future for themselves and their children.

26. Neglecting Charitable Giving

Charitable giving—it warms the heart and can also be a strategic financial move. Picture an elderly woman, a thoughtful expression on her face as she considers donating to a local charity. Many Boomers overlook the benefits of charitable giving, both personally and financially.

Donating to causes they care about can provide tax benefits while also creating a lasting legacy. It’s a way to make a meaningful impact while potentially reducing taxable income. By strategically planning their charitable contributions, Boomers can support their communities and maximize their financial well-being at the same time.

27. Supporting Adult Children Indefinitely

Many Boomers find themselves financially supporting their adult children far beyond their college years. This continued support, while well-intentioned, can drain retirement savings, leaving little for the future. It’s crucial for Boomers to set boundaries and encourage financial independence in their children.

Providing guidance and financial education can be more beneficial in the long run than direct financial support. Without these limits, Boomers risk their own financial security as well as their children’s inheritance.

28. Prolonged Work Life Without Savings

Choosing to continue working without prioritizing savings is a common decision among some Boomers. This approach can lead to a false sense of financial security, as regular income masks the need for substantial retirement funds.

Boomers might delay retirement, thinking they have more time to save, but unforeseen circumstances can disrupt these plans. Building a solid savings plan while still in the workforce is essential. Relying solely on work income without saving can leave Boomers vulnerable in their later years.

29. Prioritizing Hobbies Over Savings

While pursuing hobbies is vital for a fulfilling retirement, prioritizing them over financial savings can be detrimental. Boomers often invest significant amounts of money into hobbies, which can deplete their savings over time.

Balancing leisure activities with a realistic financial plan ensures that hobbies remain affordable and sustainable. By maintaining this balance, Boomers can enjoy their passions without compromising their financial stability. This approach helps safeguard their financial future and their children’s inheritance.

30. Overlooking Tax-efficient Wealth Transfer

Failing to plan for tax-efficient wealth transfer can erode the value of an inheritance. Boomers often overlook the importance of structuring their estate to minimize tax liabilities. Consulting with financial advisors to establish trusts or other tax-saving mechanisms can ensure more of their wealth is passed on to their children.

Being proactive with tax planning not only preserves wealth but also provides peace of mind. This strategic approach allows Boomers to leave a substantial legacy for future generations.

31. Ignoring the Digital Economy

The digital economy is rapidly changing how we conduct business and manage personal finances. However, many Boomers struggle to adapt to these changes, which can impact their financial stability. For instance, failing to embrace online banking and investing can lead to missed opportunities for growth and savings. By not engaging with digital tools, Boomers risk falling behind financially, which can leave their heirs with outdated strategies and limited resources.

Embracing the digital world not only simplifies financial management but also opens doors to new income streams through investments in the tech-driven marketplace. Encouraging Boomers to seek guidance and learn about digital platforms can bridge the gap between traditional and modern financial practices.

32. Overinvesting in Collectibles

Collectibles can be a source of joy and a way to preserve cultural heritage, but overinvesting in items like stamps, coins, or art can be financially risky. Many Boomers pour significant resources into these assets, hoping they will appreciate in value. However, the collectibles market is volatile, and values can fluctuate dramatically.

This focus on tangible assets can divert funds from more stable investments like retirement accounts or real estate. When the time comes, liquidating these collections may not yield the expected returns, potentially leaving the next generation with less financial security. Advising Boomers to balance their passion with practical investment strategies can ensure a more stable financial future for their descendants.

33. Prioritizing Immediate Gratification

Prioritizing immediate gratification often leads to impulsive spending on luxury items, vacations, and other non-essential goods. This spending habit is common among Boomers who might seek to enjoy their retirement without considering long-term consequences. Such behavior can deplete savings that could otherwise be invested for future needs or passed on to children.

Encouraging a mindset shift from impulsive purchases to planned spending can create a more secure financial outlook. By focusing on what truly matters and budgeting wisely, Boomers can ensure they leave a meaningful legacy for their families. It’s never too late to adopt financial strategies that emphasize savings and investment over short-term indulgence.

34. Overestimating Pension Reliability

Many Boomers were raised with the idea that pensions would take care of them in retirement. But times have changed, and so have pension structures. Picture a 69-year-old man flipping through his pension statement, only to realize the numbers don’t stretch as far as he hoped.

Relying too heavily on pensions without diversifying income sources—like investments or savings—can leave Boomers financially vulnerable. And when funds fall short, it’s often the kids who feel pressure to step in.

Encouraging Boomers to reevaluate the stability of their pension and plan accordingly can protect not just their future, but also their children’s financial well-being. It’s about building a multi-layered safety net, not just banking on one.

35. Avoiding Difficult Conversations

We get it—talking about money, end-of-life wishes, or inheritance can be awkward. But avoiding these tough conversations can lead to confusion, resentment, or even family conflict down the road. Picture siblings arguing over vague instructions because “Mom didn’t want to talk about it.”

Clear communication now can prevent chaos later. Boomers who open up about their wishes, finances, and plans provide clarity and peace of mind to their loved ones.

It’s never too early to start these conversations—and they don’t have to be somber. They can be empowering, honest, even bonding. The best legacy you can leave? One that comes with no surprises and lots of understanding.

36. Ignoring Digital Assets

Many boomers overlook the importance of managing digital assets. Cryptocurrencies, online accounts, and digital property often remain unaccounted for in estate plans.

Lacking knowledge in this area can lead to lost wealth and inaccessible funds. Some might have significant portions of their wealth tied in digital currencies or online businesses. A surprising number of inheritors find themselves locked out due to passwords or security questions unknown to them.

Digital asset management is becoming a new frontier in financial planning, with experts emerging to cater specifically to this need.

37. Relying on Heirlooms’ Value

Boomers may count on heirlooms to hold or increase value over time. These cherished possessions, like vintage jewelry or antique furniture, often come with sentimental attachment.

However, market demand for such items can fluctuate, leading to potential financial disappointment for heirs. The assumption that these items will appreciate or even maintain their value often proves misguided.

Market trends shift rapidly, and what might be valuable today could become obsolete tomorrow, leaving the next generation with less than expected.